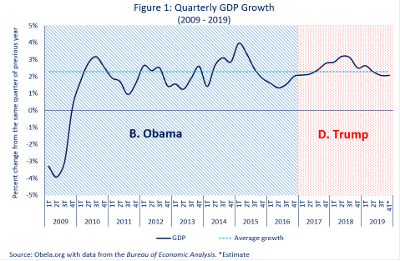

Since the beginning of the trade war, American economic growth has started to slow down. It drops from 3.2% in the second quarter of 2018 to 2.1% in the last quarter of 2019 with reference to the same quarter of the previous year, as can be seen in Graph 1. The consequences are: a reduction of the external deficit, due to less import of industrial inputs; and an increase of the fiscal deficit due to less tax collection. This situation contrasts with what the president of that country said in his appearance at the World Economic Forum (WEF) in Davos, which international press such as the Financial Times have pointed out as a speech directed to voters in an election year.

Much of Trump's speech rested on labour. It is from this data that he proclaims that the U.S. economy is in a previously unseen economic boom. The dynamism in the generation of employment is undeniable, this has led the unemployment rate to minimums that were not seen 50 years ago. However, not everything is honey on the cake.

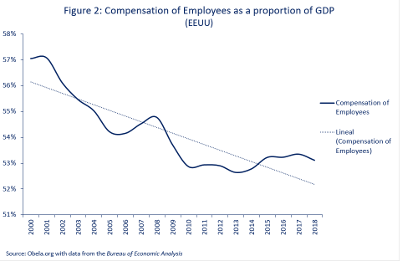

In the first place, when you look at the number of jobs generated and the unemployment rate, everything indicates that the economy is indeed generating greater welfare. By December 2019, the former reached 152.4 million and the latter had reached a level of 3.5% by the end of the year. On their own, these figures are positive, but there are questions that are relevant if we talk about an improvement for the working class. The first and most important is the employment income of all these workers in the economy. According to data from the BEA, from 2000 to 2018 the income of workers fell from 57% to 53% of GDP, as can be seen in Graph 2. This suggests that at least the real wages of less qualified workers have fallen.

This situation highlights the problem of distribution of wealth in the United States against the discourse of greater welfare for the population. One issue to be taken into account is the fiscal reform of late 2017, which led to the Corporate Income Tax revenue decreasing to 1% of GDP in 2018, a much lower level than 5.7% in 2002, the minimum since 1965 according to OECD figures.

This situation explains the increases in corporate profits at the expense of wages and taxes. On the other hand, the increases in nominal wages have to do with the logic of the labour market and not with the goodness of paying more to the working class. This aspect is best understood by looking at either the unemployment rate with respect to its natural level or NAIRU (Non-Accelerating Unemployment Rate) or the gap in output with respect to potential GDP.

The unemployment rate has been below the NAIRU for 12 quarters, indicating that the labour market slack has been fading. The result is that nominal wages are trending upwards. In terms of GDP relative to potential GDP, according to data from the Federal Reserve Economic Data (FRED) since the third quarter of 2017 the US economy has been operating above its potential level for 8 quarters, on a downward trend. These two aspects reflect the same situation.

Strangely enough, this is not leading to higher inflation but to secular price stagnation. The tariff increase should also be impacting on input prices, but this has not happened either. What seems to have happened is a slowdown in the industrial manufacturing sector.

It is likely that the U.S. economy will continue to operate in this way for some time, but it is clear that it cannot continue indefinitely given the slowdown seen in 2019 from previous years. The economic forecasts of the World Bank, the International Monetary Fund and the UN predict that the U.S. economy will continue slowing down to 1.7-1.8% annually by 2020-2021.

US manufacturing production indicators are declining according to the PMI, although, since September 2019 there is a slight inconclusive change. The Purchasing Managers' Index (PMI) is an index of the prevailing direction of economic trends in the manufacturing and service sectors. It is a diffusion index that summarizes whether market conditions, as seen by purchasing managers, are expanding, staying the same or contracting. All indications are that the economy is relying on the service sector for its weak growth while the stock markets continue their expansion, more because of the effect of negative interest rates than for their real profitability.

In this context, it is necessary to take into account that it is an election year in the United States, where there are elements with impact on the global economy: a) a much less aggressive position in aspects of international trade: for example, the trade truce with China and the signing of the USMCA; b) a much more hostile scenario against multilateralism, such as the truncation of the WTO appeals court by the United States and ignoring the United Nations Security Council in its military and political interventions abroad; and c) an expansive economic policy, with a more lax monetary policy, reduction of interest rates and more public spending on infrastructure.