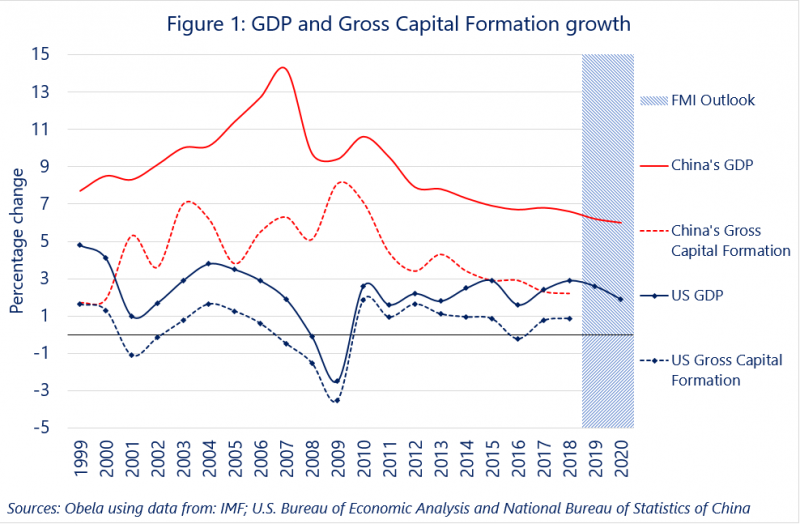

This note attempts to analyse, from a macroeconomic perspective, what we believe are the causes and consequences of economic dynamics and trade warfare from aggregates such as Gross Capital Formation (GKF), GDP and the Business Confidence Index (BCI). The Observatorio Económico Latinoamericano (Obela) has noted before some of the microeconomic reasons that from our perspective are at the heart of the dispute. Among them have been identified: the loss of productivity of the U.S. economy, technological progress and Chinese telecommunications, as well as the shift in the energy matrix towards clean energy. A central point to understand this trade war, from the macro angle, is the difference between the dynamism of the GKF between both economies. Between 1999 and 2018 the average annual growth of GKF for China was 4.4%, while for the US it rose to 0.5%, a difference of almost 4%. As can be seen in graph 1, over a 20 year period there were 6 episodes of a drop in the annual growth rate of this variable in the USA, a situation that contrasts with the case of the Asian country, where there was an annual growth above 1.9%, relatively stable.

Correlations were obtained from 2008 to 2018 between GKF and GDP growth for both economies, and the results were 0.86 in the Chinese case while for the U.S. it was 0.94. It should be kept in mind that the maximum value for correlation is 1 in absolute value. This suggests that lack of GKF growth induces lack of US GDP growth in this period.

On the other hand, lower GKF growth impacts Chinese GDP growth more than trade war. The slowdown in Eastern GDP comes since 2007 because of the fall in investment growth while no major falls are expected as a result of the trade war. GKF's performance has had an impact on productivity in both countries. An article published by the Bureau of Labour Statistics (BLS) reports on the fall in U.S. manufacturing productivity. This results in the huge American trade deficit, and the change in its export matrix, which has been reprimarised.

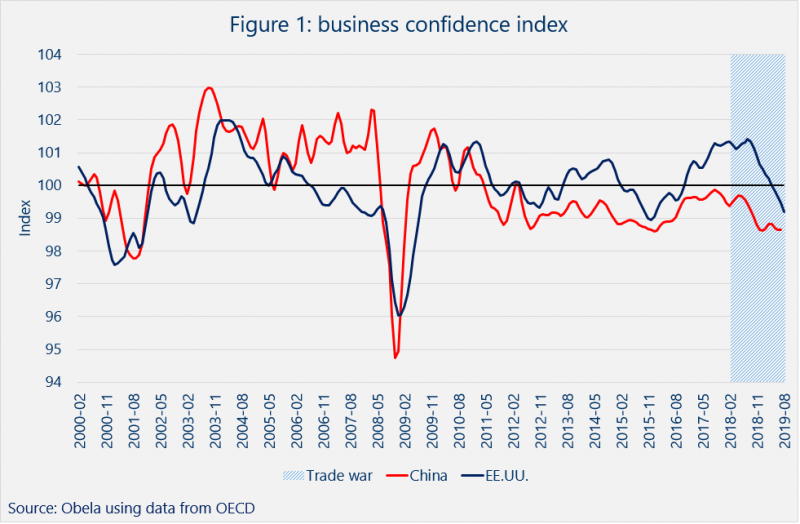

The trade war affects business confidence whose measurement in March 2018 expressed as BCI, Business Confidence Index, gave 99.5 and 101.2 for China and the U.S. respectively. (Graph 2) In that order, the last data for each country as of August 2019, is 98.6 and 99.2, a negative variation of -0.8% and -2.0%, being the US the most affected. This is reaffirmed with the report on manufacturing published by the Institute for Supply Management (IMS) as of October 1st of the current year, where American production, employment and manufacturing indicators observe another contraction.

The IMF's economic growth expectations for 2019 and 2020, usually overestimated, are that China will grow to 6.2% and 6.0%, respectively, while the U.S. 2.6% and 1.9% Contrary to what the specialized media and the U.S. president say, a slowdown that brings growth above 6% is better than an "expansion" that leads to growth of less than 2%.

The trade war is nothing more than the product of the economy of a country that was once the world commander and today, faced with the loss of competitive capacity, seeks to blame its main rival as it did in the 1980s with Japan. In a misreading by the U.S. administration, other countries are blamed, among other things, for dumping, and tariffs are thought to correct the structural problems of their economy. The truth is that with a bad diagnosis and a bad economic policy, the U.S. will not correct the macroeconomic problems it faces and has not yet been able to resolve, yet.

The difference between China and Japan is substantial. China is not Japan, it has a population four times larger, a much larger territory, it does not suffer from the trauma of the world war and for years it has followed a well-defined growth plan with a set of policies that seek to boost economic growth. Today it is already the main economy measured through purchasing power parity (PPP); it has the 5G network and seeks to position it; it has a global infrastructure investment plan, such as the New Silk Road Initiative; it is in the process of changing its energy matrix; it is the main manufacturer of electric cars in the world; and it seems that plans to internationalize Reminbi as part of opening up its economy are advancing.